I've seen many 'formulas' for determining amt of LI to buy for SAHP and a wiiiiiiiiiide range of results.

One constant in SAHP formulas: LI policy should provide death benefit amt so widow(er) can hire person(s) to perform services of parent (nanny, cook, housecleaning, tutor, lawn service, what-ev) for number of yrs the offspring would continue living at home, say, until high school or college grad.

Not to champion one formula or another, but each uses

assumptions which may or may not be well founded/reasonable in all situations and which may or may not be explicitly stated.

Was

$500,000 death benef on MS' life inappropriately

high amt to replace MS's reported $40,000 earned income?

Low? Or about right? IDK.

Q - did MS have $40,000 earned inc at time of app (~2005)? IDK,

nevertheless...

Dave Ramsey example calculates amt of LI/death benef to purchase, by assuming death proceeds will be invested at a

10% interest rate.

$400,000 death benef x 10% int annual =

$40,000/yr to employ substitute for SAHP's services. No publication date, but very stale, decades stale, imo.

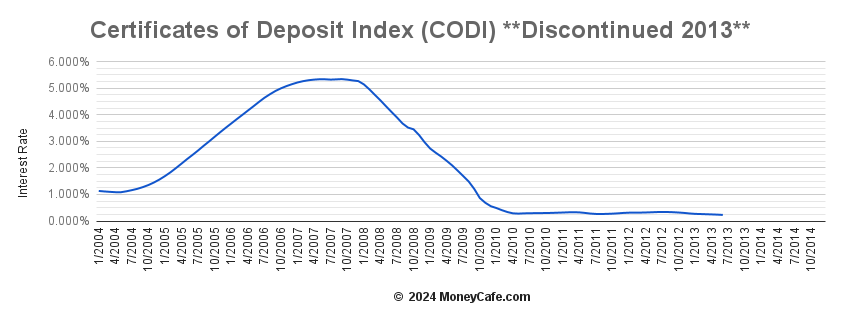

10% interest rate was a reasonable premise many yrs ago for investments such as CDs*, money market funds. But

currently expecting comparable int. rate is an unreasonable, unrealistic azz-umption.

Also one

unstated assumption in Ramsey example: - widow(er) pays ($40,000, in ex.) for these services for a given number of years & needs to have

principal intact ($400,000 in ^ ex) at end of period. May or may not be the case.

End rambling. All ^ JM2cts.

____________________________________________________

*

chart below from http://www.moneycafe.com/personal-finance/codi-rate-certificates-of-deposit-index/

Chart shows 2004-2013, 10% int rate not remotely avail in that period. Links below show other periods.

https://research.stlouisfed.org/fred2/categories/121

http://www.ratestracker.com/historical-cd-rates/